Learning to balance our money and be responsible, is an important lesson to learn. Balance in all things is what we are trying to achieve here. Since this is a major factor in our life, I decided a post was in order. Not to worry, it will not be all physical- for currency is also a thing of heaven. There are a couple of things I have learned that are key when you are learning about how to balance your finances. Even better, I have gone ahead and created a PDF printable sheet you can print and laminate and use with a dry erase marker for your monthly needs!

Needs vs Wants

One of the first things to get in order is to know the difference between a need and a want. Your definition of a need and want is crucial to know for your financial success. A need is something to sustain life, something necessary, a basic need to live humanly. Basic food, water, hygiene, and sleep. Now, there are levels each of these… there is basic and then there is splurging. Splurging is good I believe, but all in a balance, and if the funds are there. Lets talk about that…

One of the first things to get in order is to know the difference between a need and a want. Your definition of a need and want is crucial to know for your financial success. A need is something to sustain life, something necessary, a basic need to live humanly. Basic food, water, hygiene, and sleep. Now, there are levels each of these… there is basic and then there is splurging. Splurging is good I believe, but all in a balance, and if the funds are there. Lets talk about that…

Do you NEED and $60 steak to survive? Or can you live on a $5 meal? How much does a basic meal cost you? I know I can feed my family of 5, eating out for $25. I can also go cheaper cooking a lentil meal at home for under $10. We can also go out to eat for $50-60 bucks easy- and splurge. What is basic meal to you? Water, and hygiene are the same as well. There is expensive water and there is basic generic brand water. Expensive toothpaste and basic toothpaste. If money is tight you go with the basic generic brands and only with the basic needs to sustain yourself.

Lets talk about cars, do you need a car? Can you do public transportation? If you say a car… do you NEED a Mercedes or a $2000 car? Get your needs and wants straight and this will help you with setting healthy priorities. Wants are all the extras and fluff. The nice things to have that make life easier, but not necessary to sustain it.

Positive or Negative

Next, everyone either has a positive or negative relationship with money. What are you? Do you see it as evil? I think this quote is true:

Money is not evil, it is the love of money that corrupts

It is all about where your heart desires and intents are. Usually someone that has a toxic relationship with money, has a  blocked flow in their giving and receiving. One thing I know is the law of giving and receiving. There has to be a flow in your life of money or you will always struggle with it. If you hold onto it SO tight, you will loose it and never seems to have enough, always slipping through your fingers. If you always hand it away without any thought, you will always have the short end of the stick and people take advantage of you. There must be a balance in your life of giving and receiving. Do not take, take, take and do not just give, give, give.

blocked flow in their giving and receiving. One thing I know is the law of giving and receiving. There has to be a flow in your life of money or you will always struggle with it. If you hold onto it SO tight, you will loose it and never seems to have enough, always slipping through your fingers. If you always hand it away without any thought, you will always have the short end of the stick and people take advantage of you. There must be a balance in your life of giving and receiving. Do not take, take, take and do not just give, give, give.

Abundance follows Joy

Having abundance comes from heaven, for in that space nothing is lacking. It is always the best of the best. If you realize your abundance directly correlates with you living your joy and being authentic, you then realize the power to change lies with only with one person- you. We always need to point the finger at ourselves if we want something to change. Also, realizing it is not ALL on your shoulders helps too. I have written a post on the book called The power of the subconscious mind, this book will help you re-program your mind and change your relationship with money.

There is currency in Heaven

1 Peter 1:7- That the trial of your faith, being much more precious than of gold that perisheth, though it be tried with fire, might be found unto praise and honour and glory at the appearing of Jesus Christ:

Even though I do not believe there is “money” in heaven, there is a currency we can trade with for things. Here is says: the trial of our faith is more precious than gold. Faith is already a gift from God, and as it gets tried and becomes stronger and stronger we can trade that back into heaven for other things we need. There is always a giving and receiving with heaven as well. You can trade and give up something like food for a day, bad habits, your time and your agency for things of a better from heaven.

Back to Basics

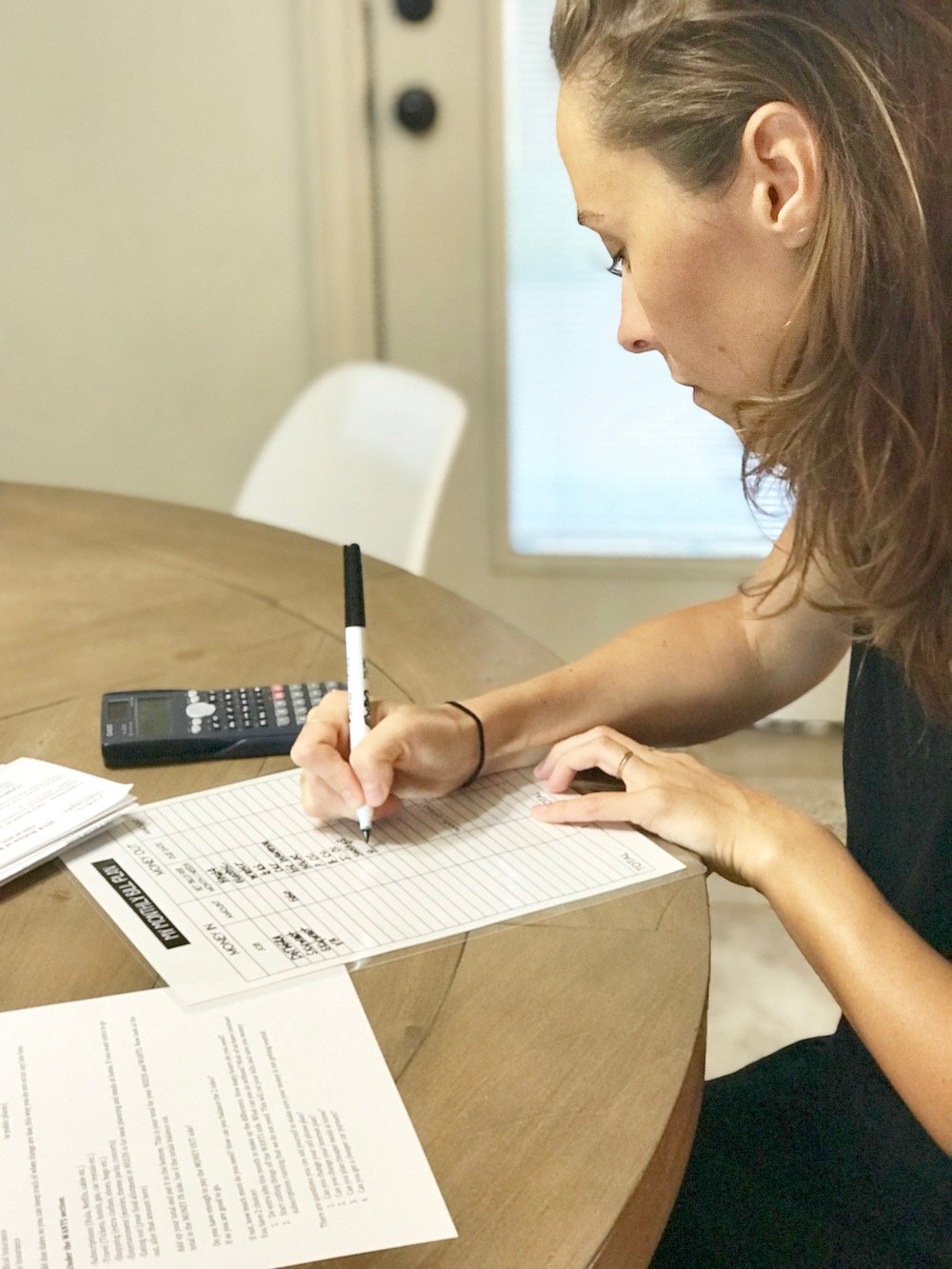

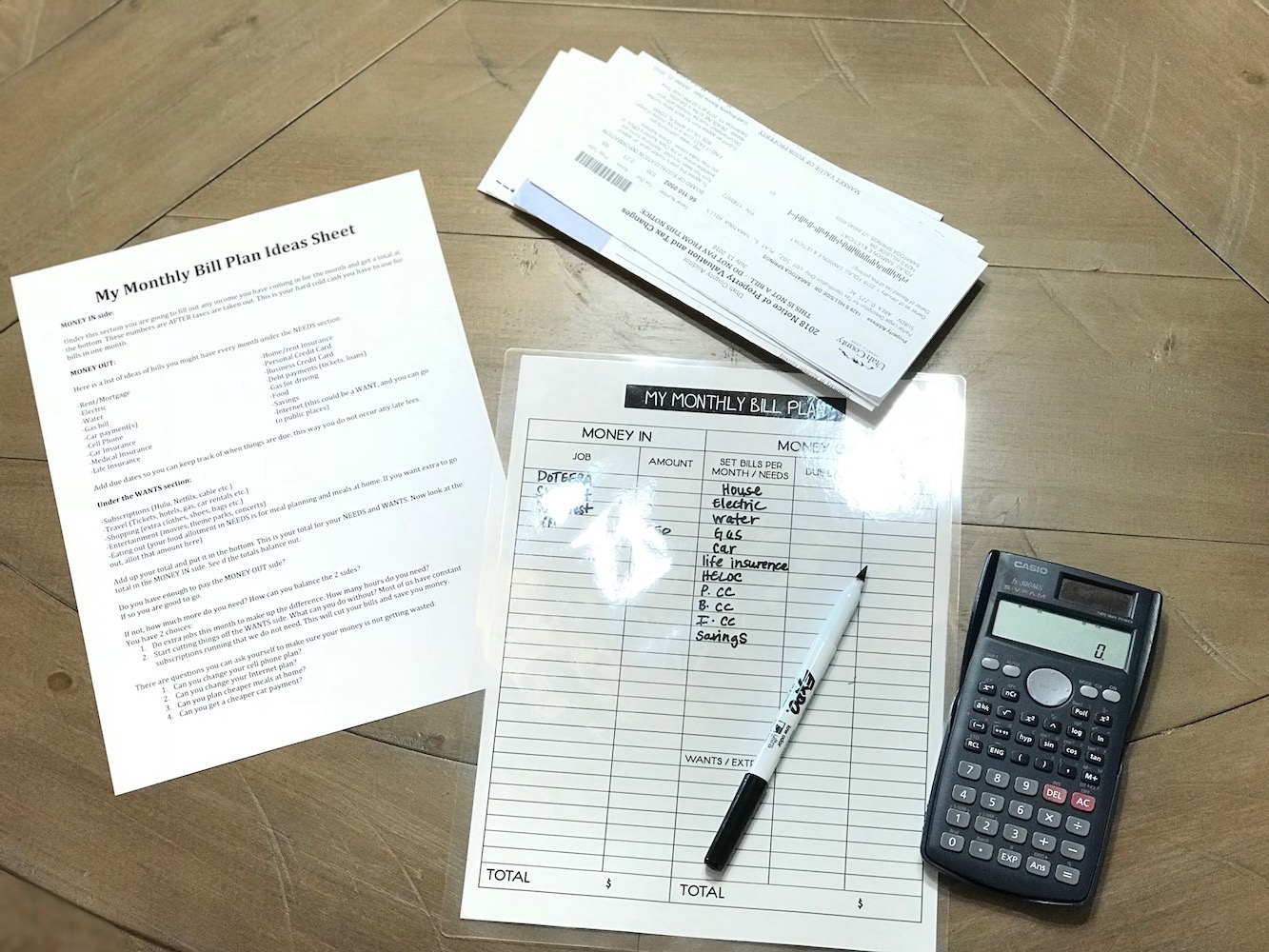

OK finally, onto the printable sheets! It always helps, at least for me, to see something physical and in writing. To see it right in front of me. This is the basics: this sheet will help you see the money you have coming IN vs the money you have coming OUT. You can see it plain and simple. Then you can come up with a plan to BALANCE the two sides.

OK finally, onto the printable sheets! It always helps, at least for me, to see something physical and in writing. To see it right in front of me. This is the basics: this sheet will help you see the money you have coming IN vs the money you have coming OUT. You can see it plain and simple. Then you can come up with a plan to BALANCE the two sides.

- The first sheet goes through and gives you ideas of what you might need to include in your monthly bills. There is an explanation and ideas given of what might go in the needs vs wants sections. And then after seeing your totals, there are some questions to ask yourself, to help you come up with a plan to get the two sides into balance. Here is the sheet: Monthly Bill Plan Explanation.

- The second sheet is the one you want to email to your local copy store. Ask them the print it and laminate it in THICK laminate so that you can use it for a long time and it will not be flimsy. This cost me $3.50, no big deal right?! Then you get a fine tip dry erase marker and get to work! Here is the sheet: My Monthly Bill Plan.

Debit Card, Credit Cards and Checks

Lets have a little excerpt on the differences between credit cards, debit cards and the pros and cons of each. Knowing some key things can make a huge difference in making your life easier or more difficult. Credit cards can be a blessing or detriment depending on your knowledge of using them. So lets start:

Debit Cards

This card is simply a piece of plastic instead of carrying all your cash. Writing a check is the same thing as using your debit card, except that it is faster and you do not hold up the lines. Both ways do not build credit and depending on your account, you can not use more than you have of hard cold cash in your account. You deposit your money in your account and then simply use the card to take out the money when you purchase. There are no rewards with these cards, and when your money is gone your card will no longer work. So do not forget to keep making those deposits 🙂

Credit Cards

A credit card is given based on qualification and your credit score. Also looked at is how much income you have coming in. You are given what is called a line of credit. This credit card is not based off of money you already have or “hard cold cash” but essentially is borrowed money from the bank. This means that if not paid back, you will pay interest for your borrowing of the bank money and usually that is 18-25% of what you borrowed. This is wasted money on your end and should be avoided.

If the money is not paid back at all, and your can not make payments, your name is sent to the creditors for collection. Your credit score to your name is also ruined. If you still can not pay, you will have to claim bankruptcy which will forever be on your credit score. This is the dreaded curse of credit cards.

There is way to avoid credit cards being a curse, and turn them into a blessing. Here are a few tips to follow:

Your credit score is how you are able to take out loans. Loans to buy a home later in life, qualify for rent, buy a car and bigger things like that. If you do not have a good credit score you can not qualify for these things. Your credit score should be between 750 to 800+ to be considered good credit. This way you can qualify for loans and have lower interest rates. Your credit score is something you want to build, not destroy, and it will help you.

Credit Card tips:

1.Always pay off the FULL amount owed. They will tell you, you only owe a “minimum balance” and you do only owe that. But do not pay it. They do this so that they can get more money from you and so they can charge you interest! Your main thing to understand and do with credit cards is: do not spend more than you have.

Lets do an example:

If you have a credit card with a limit of 5,000, that means you can not go above that, but if you do not have $5,000 to pay it ALL off in a month then do not spend that much. Only spend what you can pay off in FULL in one month. If you use $500 of the $5,000, you now have a limit of $4,500 to use. Once you pay off that $500 in a month, your credit limit goes back to $5,000. If you can not pay off the full $500 used the will charge you interest of that $500. If your interest is 18% that means you pay $90 to them just for using their money. That is $90 more dollars of your own money that could have been used for something else.

2. Get a credit card with rewards. I get back anywhere between $500 a year from what I spend on my credit card. That is free money! There are other options like: miles for free flights, hotels, gift cards etc. Pick one that will best benefit you.

3. Use as cash. Any bills you would pay in cash with your hard earned money, put it on a credit card instead and then use the cash to pay off the FULL credit card. This way you build your credit score, earn free stuff, and do not have to carry around all the cash. Do not think a credit card is “free” money and you can use as much as you want. See it just like cash.

Hope this helps bless your life and make it easier! Shifting into being able to have a good relationship with money, will help you be on your way to living a High Vibe Life.